James Halstead

A stock pick, but not one I own just yet. Mainly just a breakdown of a business I like. Of course, with sprinkles of my own investment philosophy :)

Ideas are overrated. A couple of solid ideas a year are more than you need. The human mind, however, would rather keep turning over new rocks (rightly or wrongly) and fail to stick to what it knows.

Chasing alpha viz. getting greedy with the returns you desire, in my view and experience, is a surefire way to destroy a portfolio. It is only through sensible, non-speculative security analysis that one can compound returns for a long time. In my experience it has also been that risk and reward are largely correlated. You may hit three ten-baggers but three successive failures will wipe out a portfolio. And mentally destroy you.

At the time of writing it had been four months since my last pick (which I traded out of) and I suspect between this and my next writeup there will be a significantly longer gap (that I will try to fill with musings and commentary).

Please don’t expect any “big” picks in 2026 unless the market crashes. For the sake of transparency, my current portfolio is made up mainly of one company - Hardide, which I wrote up 5 months at an average price of 7.4p - and a few other small tracking positions.

Today’s pick is one I don’t own. But one I have traded in and out of.

What I’ve found is that sometimes the best opportunities come from the most unsexy businesses with no internal catalysts. Being “contrarian” does not mean always mean sifting through companies that are on the brink of bankruptcy looking for an “easy” double or triple. It can mean sifting through an industry in distress looking for a gem that shouldn’t have been whacked along with the duds.

Usually, this does mean cyclicals which many investors, understandably, are terrified of when market conditions look bleak. But in order to fully understand one business it’s important to understand the position of the whole industry. Not because competition matters that much in these industries, but to gain an understanding of what’s going on.

Currently, the flooring industry in the UK seems to be struggling. Public companies like Victoria PLC and Headlam PLC are going through complex restructurings with their share prices falling 92% and 84% in the last 5 years on the back of a macro slowdown, primarily due to inflationary pressures and higher interest rates. A glance at the balance sheet and a scan over plans for the future convinced me that the future prospects for both of these businesses were only going to get worse. Acquisition-led growth inflates shareholder value in “free capital” conditions but it’s when market conditions tighten that the market realises that they overleveraged, overpaid and destroyed value.

Another public company in the industry, Likewise Group, seems to be growing fast - but they haven’t really achieved scale. At 1.5x book value with little excess cash and 48x trailing earnings in a cyclical, commodity industry, it’s a pass. “Growth” in an industry where anyone can enter just isn’t really that important to me. It just messes up the maths for a prospective investor. And revenue growth coupled with a profit warning makes it more uncomfortable.

Simple cash flow “to me” maths is what I care about. Whilst “narcissistic” in other fields, “I” and “my” is all that matters in investing.

As for international players, Mohawk Industries seems to be a significant player and they’re also struggling - trading at 2/3rds of sales and a little more than TBV. Revenues have (somewhat) held up but margins have been squeezed hard since 2022. Returns on equity are around 5%, returns on assets are around 3% and returns on invested capital hover around the risk-free rate.

My point here is simple - there’s no pricing power in the industry and when conditions get tough, size doesn’t matter.

Of course, there are private flooring companies in the UK. And this is perhaps where the intelligent investor should maybe focus more. Poor governance through terrible capital allocation and weak boards is especially rampant in UK PLCs and maybe less likely to be the case in private companies where directors may be more aligned.

Tapi Carpets & Floors Ltd are one to watch closely. Following the acquisition of Carpetright out of administration for £10.4m, Tapi’s revenues grew 33% and pre-tax profits nearly doubled from £9m to £17.7m in 2024. Challenging conditions have always provided opportunities for those able to act swiftly.

However, even private companies are struggling with many reporting declining sales and profits on Companies House. (Of course, there’s a large time lag between reported figures and the filing of accounts.) And let’s be even more frank - after scanning a few financial statements, you quickly realise that none of these British companies will be the “lowest cost supplier” of flooring products due to high energy costs and expensive labour costs.

Nevertheless, customers are irrational. They will stick to what they know - strong past results will result in more orders. Why go shopping from a Chinese competitor?

So where exactly are we in the flooring cycle?

Well, it’s always difficult to say with these things without the benefit of foresight. However, retail spending appears to be weak, the construction sector seems to be contracting, the housing market is cooling and interest rates have not been cut enough to be stimulative.

For a company that’s not completely floundering and is able to manage their own fate - without creditors and lenders circling - this could provide the opportunity of a lifetime.

Enter James Halstead plc (AIM: JHD).

No different to any of the other players:

Our model is to manufacture in volume, high quality flooring that we sell to distributors and stockists to satisfy local demand whether this is via third parties (as in the UK), via our own businesses across the globe or into direct export markets.

Ok, translation - JHD manufacture flooring. In the UK especially, the company sells in bulk to wholesalers and distributors rather than direct to end-users meaning distribution of their flooring is mostly via third-party distributors and stockists. Internationally, they have subsidiaries and distribution partners in many countries and also export directly.

James Halstead specialises in vinyl flooring solutions under their flagship brand, Polyflor. They have pioneered eco-friendly initiatives like the Recofloor recycling program and operate globally, supplying flooring to healthcare, education, retail, and transport sectors.

Recall Headlam from earlier who “is the UK’s leading floorcovering distributor.” Therefore, Headlam are a proxy for the kind of JHD customer. And despite downsizing strategies to focus on the core and focus on their customers, their business is a mess. The company is reducing stock, selling off excess property and expects 2026 to also be loss-making. James Halstead depends on healthy distributors that have the ability to take their inventory.

Once again, we turn to the private companies where there is a time lag to “feel” for what’s really going on - Columbia Flooring and STS Flooring Distributors seem to be large competitors to Headlam that may also supply JHD flooring to customers.

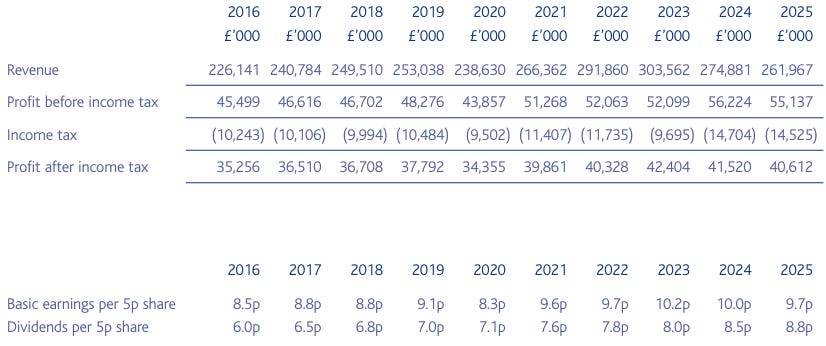

The best businesses are the ones that have some certainty to them. A coupon element. So predictable they’re bond-like. James Halstead is this. Despite revenue declines in the last two years the profits remain steady.

FY2025 for JHD

In the above sections, I wrote about how other UK flooring companies are struggling. Well, James Halstead reported growth. 1% growth, but growth nonetheless. And when others are shrinking, the net effect is higher.

Outside of the UK, French sales fell 20% with distributors reporting revenue down 15-20% leading to price discounting, and with independents struggling there has been an element of consolidation in the market. German sales fell 3.2%.

In Australia, sales fell 9.3%. The economy remains weak with low growth and a continued cost of living crisis. Real wage growth has remained negative which has impacted the housing market with new builds/approvals subdued. On the back of this, sales of products in domestic and retail markets have struggled.

Furthermore, in New Zealand, demand has been weak. JHD benefited over the past years from government policy of building new social housing, but this has ended. Whilst there will be some remedial /refitting work, it will not be on the same scale and over the past 12 months JHD restructured the business, closed the Christchurch warehouse, reduced staff numbers and sublet unused areas of the Auckland warehouse and refining territories.

The North Asia business, now relocated to Shanghai with a satellite office in Hong Kong, remains subdued. The slowdown in the construction market has left flooring manufacturers that supply these markets short of demand resulting in competitive pressures. Whilst the pipeline of orders is improving, they have lacked larger volume projects. Rebuilding market share continues.

Whilst there are challenges, JHD is a global business that has diversified itself well to benefit from recoveries in other nations - namely: Canada, Malaysia, Brazil, Mexico and the Middle East.

Why JHD is Different

Investors tend to be quick to praise the benefits of operating leverage (ie high fixed costs such that revenue growth results in faster profit growth). And it’s true that operating leverage works as long as a business grows. But operating leverage in a cyclical companies is risky because you can be damn sure that at some point the growth will reverse. How will you take the costs out and stem the bleeding of cash? Most won’t be able to without hacking off an arm - especially when there’s financial leverage involved. And which rational investor wants to buy a business that has a dilemma between self-harm or cancer?

Therefore, a cyclical whose costs can vary in line with demand becomes much more valuable even if it’s upside is capped in boom times. Investors tend to fall in love with operating leverage companies because - just like a stock that’s fallen 90% - the returns always seem unlimited if just a few things go your way. But that’s irrationality allowing greed to talk.

It’s akin to buying a oil company with a $70/bbl breakeven cost that refuses to hedge their output to “maximise” returns because oil “has to go up at some point.” It’s economically illiterate to get involved with these kind of companies forever. Worse, management - entirely through luck - can have impressive track records that investors treat as genius, resulting in a poor operator holding on to their job for far longer than is appropriate.

Shareholder Returns

Anyway, JHD trades at 14x earnings at £560m with £60m excess cash. On an EV basis, it’s about 12.5x earnings with a 6.5% dividend yield. Unfortunately, I will miss the dividend this year as I built my position quite recently only to trade out of it following a bump. But I’m ok with that. JHD have a track record of increasing their dividend and maintaining a high payout ratio.

Some investors will feel uncomfortable with such a capital allocation policy. But I view it as very disciplined. Return 80% of profits to shareholders, maintain a cash buffer, don’t pursue growth for the sake of growing… it comes across as very, very intelligent and stops management from doing dumb things.

Furthermore, this is a business that won’t change so much. In a century, I’m sure the world will need floorings somewhere in some form. With small but consistent innovations - as has happened for many decades - JHD should be around at that point if they continue to operate the business in the same way.

Going back to shareholder returns, assuming the dividend remains constant it will take about 16 years to recoup your initial investment - assuming zero dividend reinvestment. However, it gets more interesting if the dividend remains constant but you reinvest. I’ve bought these shares into my ISA. Therefore, at 6%, given that I won’t receive a dividend this year, it will only take me 13 years to double my initial investment. If we further consider dividend growth - which has averaged 4.5% over the last decade - an initial investment of £100 turns into £287. Of course, this assumes no tax and no transaction fees (and no share price appreciation, either!).

My point, that the most layman of investors understands, stands to reiterate something crucial - dividends, not share appreciation, are where your compounding can come from. It’s far easier to map out and yet people rarely talk about it.

The reason why investors may not think in this way comes down to way too much focus on share price charts and not total return. In fact, JHD’s stock chart paints a bleak picture. In the last 5 years, the stock is down 40%. In the last ten, it’s down the same amount.

I can hear someone saying “If you invested in 2012, you’d have made no money!” which is blatantly false. Think about it like this - the principal hasn’t changed in value but the interest payments have kept coming through the door. It’s really not so bad! Speaking of dividends, fun fact: JHD have managed a dividend increase in every year for the last 50 years! (Although, part performance is not indicative of future returns.)

The issue is that investors would rather look for something “ obviously mispriced” and “cheap” that may double overnight or something GARP-y that should continue growing. Both of which usually err on the side of speculation. I was the same. But why make investing unnecessarily difficult? It’s hard enough as it is!

Furthermore, the JHD business seems to be highly efficient. A net margin of 15%, a pre-tax margin of 20% and a FCF margin of 10% in this industry is impressive. (Note FCF is defined as cash from operations less PP&E additions less lease costs.) All of the above equates to a ROE greater than 20% - and ROE is an appropriate measure here due to the debt-free balance sheet and the fact that the industry is struggling. This is not “peak” ROE which was 27% in 2021. However, the fact that ROE is consistently healthy shows the strength in the operations.

The reason I don’t use “cash” ROE is because the nature of the business is such that working capital changes skew the cash flow dramatically. It’s true we could adjust for such working capital movements by reversing them but mixing accrual accounting with cash accounting has never made that much sense to me. Tracking cash flow is important obviously but I prefer to not scrutinise it too much unless there are glaring red flags (receivables/inventories/payables mismatches etc).

Generally, cash flow generation has been solid with cash flows in line with profits - that said, in FY2022 James Halstead made the classic “inventory” blunder that so many others did and they continue to navigate that issue.

And what I’ve failed to talk about is the optionality that £60m cash gives. JHD haven’t pursued this strategy (yet) but if conditions deteriorate further they may be able to use their surplus cash on acquisitions, cheap rent or upgrades to their equipment. Whilst competition enters administration, JHD’s conservatism pays off in a large way. Therefore, you really get a 6% yield plus optionality.

Some investors will be worried that the high payout ratio is a feature of a mature business with low growth prospects and slower compounding which could be true. After all, the payout ratio has increased from 40% in 1996 to 90% in 2025.

However, I’ll cite the annual report here:

There is no doubt that we have faced challenges... The malaise in Central Europe due to low customer confidence continues to affect shop-fitting and retail premises with cuts to renewal and roll-out programmes. We shall approach the short term with caution, tight cost control and a conservative approach to customer credit. The latter being particularly important as competitors in thin markets chase volume. I remain confident that our portfolio of products is appropriate to the marketplace and of continued overseas growth backed by a robust market share in our home territory.

The boldened section about caution is incredibly wise to me. There are very, very, very few CEOs that would actively abstain from revenue growth.

Furthermore, the strategy is set out very clearly:

The board continues to consider growth in profit before tax and growth in dividend key targets in line with the task of delivering shareholder value.

My point is that I’ve read/heard critics say that James Halstead is not a “growth” company and I couldn’t disagree more. It’s only now that revenues haven’t really grown that critics get frustrated.

Management

I haven’t really spoken about management because there’s not much to say.

Mark Halstead was recently appointed Executive Chairman last year having been with the Group for over three decades. Gordon Oliver was also promoted CEO, having been made CFO in 1999 and Financial Controller in 1987. David Drillingcourt was made CFO having been at the Company since 1996. I cannot really fault them in terms of strategy and I want them to keep running the company as they have been.

The John Halstead Settlement controls 17% of shares outstanding suggesting the Halstead family remain invested in the business. Furthermore, non-Halstead management seem aligned and have made small purchases recently on the open market. It also is worth mentioning that management have 3.7m options with exercise prices significantly higher than the current market price around the £2 mark (c.50% above current market price) which begin to expire in the next two years.

What this really comes down to is focussing on downside viz permanent impairment of capital. It’s very hard for macro to affect JHD is a severe way with their balance sheet and operational efficiencies. Perhaps the valuation looks on the heavier side but it’s proved to be a very stable business when you focus on cash returns and ignore what/how the business looks.

In terms of insufficient returns, this is usually a trickier risk to consider. Is the timing right? Is inflation going to erode my purchasing power? Again, I point to the balance sheet. You have a business that generally grows its dividend currently yielding over 6% - higher than the risk-free rate. Of course, this fails to consider share appreciation (or the opposite). However, for the investor that truly believes they’re parking their cash for the long-term, it’s not really an issue. Markets can swing and do what they do, but it’s just a paper loss/gain. Remember, cash is reality.

Business Model

This is sounds well and good, but what’s JHD’s secret sauce that allows them to stay so competitive in the face of dire economic conditions? Early on, I thought JHD might be a fraud given the high margins and net cash in a tricky industry. (Since I did not want a Patisserie Valerie situation on my hands I took the time to figure it out.)

The first element is vertical integration. James Halstead designs and manufactures flooring in its own plants, then sells under its own brands. Maintaining manufacturing capacity lets them control formulation, quality, throughput and yields. The result is a lower variable cost per unit at scale, better control of input sourcing and faster product development / premium SKUs without relying on outsourced manufacturers who take margin).

UK peers like Headlam are more distribution-heavy rather than manufacturer-centric, showing materially lower gross margins than a specialist manufacturer with proprietary product lines.

The second element comes down to product mix with a focus on specification-led, higher-value commercial ranges. James Halstead focuses on commercial resilient floors and higher-spec product lines (technical/conductive, acoustic, premium LVT ranges such as Expona/Polyflor). These are often specified by architects/consultants rather than bought as commodity retail.

Distributors or mass-market flooring retailers compete on price and volume - lower per-unit margin and more exposure to retail cycles. Halstead’s product focus is higher up the value chain.

Furthermore, it is a relentless focus on cost control that makes James Halstead so valuable. Take these passages from the most recent annual report and note the candour:

Overheads, at all levels, were targeted throughout the year. The decision was taken to delay the recruitment of replacements for leavers across all departments and there was a key reduction at the board level of the business with three director/executive level people leaving and a resultant restructure within the existing teams. Marketing spend was refocused to target grass root demand by a series of promotions targeted at the independent contractor to push demand to the distributors and a series of promotions to the end buyers of our products to encourage larger deliveries of key product lines to stockists.

Plant efficiency and manufacturing output are crucial to the performance of our (UK) business. With overheads such as energy continuing to exceed those of our international competitors, (UK) production lines have continued to seek process improvements and increase machine utilisation to reduce the costs per unit of output. We are, in the coming year, looking to address manufactured volume sales in the Australian market by investment in the grass roots areas of education and healthcare.

Risks

The risks here are intuitive -

Multiple compression - JHD is just a flooring company. 14x earnings could be deemed expensive by the market despite the high payout ratio. There’s no reason why the multiple doesn’t compress to a HSD/MSD multiple - irrational that may seem.

Macro gets worse - JHD is a global player but if inflation creeps back up or customers ease on spending JHD suffer.

Costs can’t keep getting taken out as revenue falls resulting in worse EPS and a dividend cut.

Catalysts are not clear. We can hope for better market conditions. However, there was one interesting resolution I noted for the upcoming AGM:

Resolution 13 seeks to renew the authority of shareholders to allow the company to purchase its own shares in respect of up to 10% of the issued capital at prices not exceeding 5% above the average of the middle market quotations for the five business days preceding the purchase. The directors undertake that the authority would only be exercised if the directors were satisfied that a purchase would result in an increase in expected earnings per share and was in the best interests of the company at that time. The directors may choose to hold shares purchased under such authority in the form of treasury shares (subject to a maximum of 10% of the issued ordinary share capital at any one time).

Some may think I’m confusing stability with attractiveness. JHD is a dividend play. But what if flooring is a race to the bottom with shrinking end markets whose only good quality is that they don’t screw up as much as competitors?

It’s a possibility, right?

However, as JHD write in their annual report -

Electrostatic dissipative (ESD) floorings have been a part of our ranges for many years particularly SD (static dissipative) and EC (electro conductive) flooring. During the year we have invested in our plant in Radcliffe to upgrade these ranges to add focus to these products as they are used in server rooms and areas of high-end electronic equipment, and this is a fast growing area as the world of cloud computing moves into the age of AI. We are already supplying this sector with the same flooring that has been used in hospitals for many years. The recent announcement of investments such as “Stargate UAE” and the “AI growth Zone” for the North East we will see continued growth in these products. This bodes well for sales and ongoing work by our development teams.

Ok, so it’d be a massive stretch to call JHD an “AI play” but they certainly have some favourable market trends. If one believes that we’re moving to a more technology-driven world, meaning more data centres and labs, JHD stand to benefit from the buildout. Who’d’ve thought it?

Inconclusion, James Halstead is a boring business in a commodity industry that faces challenges. However, with competent management, disciplined capital allocation and strong operations, they seem to have the optionality to pursue growth in a way they seem fit. I do not know in which form this will take but a wise investor once said the best catalysts tend to be the most unforeseen ones.

As for me, I’m a stingy *fill in the blank*. Of course I’m waiting for an even better price. 10% dividend, anyone?

Best investing,

HV