Berkeley Group PLC

Finding value in mid-caps. It's been a while!

Berkeley Group is a UK homebuilder focused on brownfield regeneration (brownfield land is previously developed land that’s no longer being used, including disused industrial estates or factories) that trades on a trailing earnings yield of 10%, a forward P/E of 11x and roughly book value.

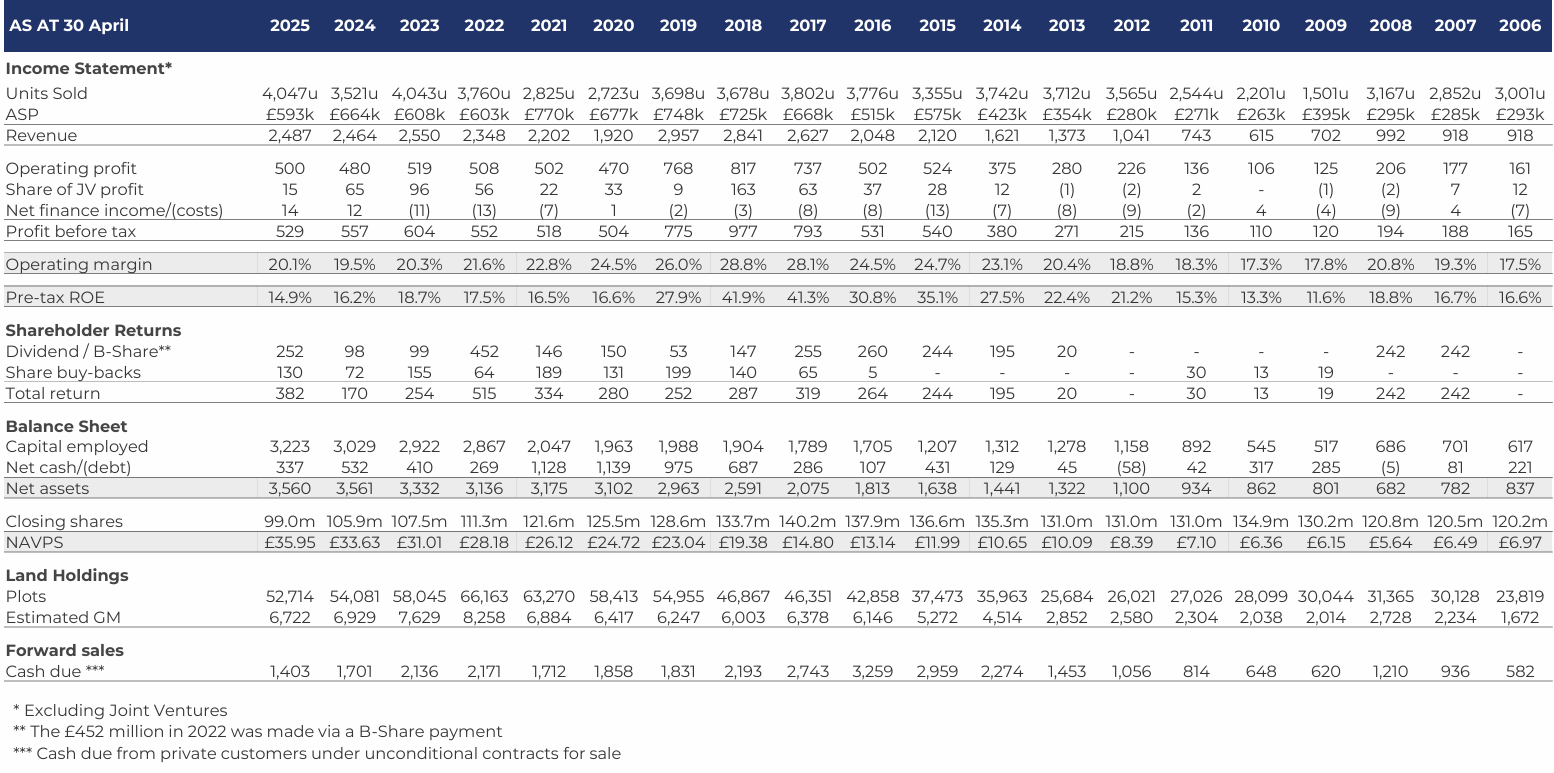

See their impressive 20 year track record below and note the consistent profitability:

It gets better when you consider management’s anticipated GM of £6.7 billion in the land bank at a market cap of £3.6b with net cash. (Although, in this industry it’s very hard to count cash as your own since management will always be keen to deploy it on land where they can.)

Two pieces about Berkeley specifically stood out to me -

Firstly, the geographic focus on London makes sense to me. London house prices typically appreciate faster than the rest of the UK due to consistent high demand coupled with shortages of rentals. However, London has underperformed since 2016 following Brexit and Covid.

I view the underperformance of London as temporary. A reversal in WFH behaviour could potentially trump affordability concerns (i.e shorter commutes is better than less sleep in a bigger bedroom). Further, London is home to some of the world’s top schools and universities meaning talent will always be in swaths around London looking to get their foot in the door. And, despite anti-immigrant propaganda, London remains the UK’s biggest magnet for globally mobile workers.

Whilst it’s true that London gets lots of bad press due to public concerns (crime, antisocial behaviour, homelessness), these problems are fixable. If 1970s New York could be turned, London certainly can. The location (financial district, nightlife, culture) is simply too important meaning it’s unfeasible to write off London. A bet on London flourishing (which is highly likely with a long-term horizon) in turn means a bet on London property prices increasing.

Berkeley feel a similar way. With a track record of “being greedy when others are fearful” and vice versa Berkeley returned to buying land last year after a two year sabbatical.

Secondly, brownfield regeneration has its perks. Brownfield sites tend to be in or near existing urban areas meaning there’s naturally more demand compared to the typical homebuilder and UK national policy pushes councils to prioritise brownfield delivery.

The cons are obvious. It’s complex. High upfront spending (remediation, planning, land assembly) and long pre-construction phases result in more time, more working capital and higher financing exposure than a typical volume site.

Despite these challenges, Berkeley Group was named the UK’s number one homebuilder in 2025 for build quality by HomeViews, the only independent review platform dedicated to residential developments in the country.

As usual, there’s a twist. Whilst the “cheap” accounting misleads you to the “right answer”, the reality is more nuanced —

Reported profits of UK homebuilders can look impressive, but they miss the most important economic cost: the return investors require while their capital sits locked up for years in land and WIP. To understand real performance, you have to revalue earnings after charging this “time” cost.

The correct lens is simple:

Identify the capital actually tied up.

Apply the company’s Cost of Capital (COC) to it.

The most accurate capital base is Average Capital Employed (ACE) because it reflects the net funding from shareholders and lenders. It excludes customer deposits and long-term land creditors, which are effectively free financing. ACE represents the pool of investor capital that must earn at least the required return.

The COC - here, a punishing 12.5% discount rate - captures the risk and duration of multi-year regeneration projects. Applying this rate to ACE produces the annual “capital charge” that should be deducted from reported profit to reveal the economic return.

Once this adjustment is made, the picture changes dramatically. For FY2025, the capital charge absorbs most of the reported margin, cutting a 27% accounting gross margin to around 11% and reducing a 16% “headline” pre-tax ROCE to roughly 3% (post-tax).

In other words, much of the profit reported under accrual accounting is simply the required reward for waiting. And here strong accounting profits leave little surplus once ongoing reinvestment in land and construction is funded.

However, on the exact same framework, looking back to the period 2015-19, Berkeley on average earned over £325m post-tax, pre-working capital adjustments (compared with £75m over the last two years). That’s the proof that this is not a bad business!

The bleak reality for Berkeley is that their capital base has swelled whilst their turnover has stayed the same. So whilst the obvious point to make is on margin compression (GM from mid-thirties to mid-twenties), it’s the WIP that’s grown 82% between 2015 and 2025 and the average capital employed swelling from £1.3b to £3.1b in a decade - whilst revenues have only grown 1.6% CAGR - that should really strike.

Cash due on forward sales (under unconditional contracts) has also decreased for three years straight - and in an inflationary environment the net result is worse - from £2.2b in 2022 to £1.4b.

As with any business, “through-the-cycle” cash flow is the true measure. To reiterate my thesis, we’re close to trough conditions in terms of both Berkeley’s ability to build and sell at the best prices.

The accounting doesn’t get less complicated here -

Land purchased for development is recorded at cost. Once moved into production, development costs are categorised as WIP. Units completed but not yet sold are included in inventory as completed stock. When a property is sold, the corresponding expenditure recorded in inventory is expensed through cost of sales. However, the nature of the business model is that it is common for Berkeley to sell homes before they are built, a practice known as forward selling. Management says their “customer deposit strategy remains 20% for forward sales.”

Furthermore, deposits are typically collected when the customer enters into an unconditional contract for sale, usually taking place during the early production phases, years prior to completion.

Of course, this alludes to the problem discussed earlier. When a builder bills revenue so early on in a multi-year development, they leave themselves exposed to build cost inflation. And there’s no evidence to suggest that Berkeley’s contracts contain explicit price escalation or price-hike clauses for forward sales.

However, the poor performance seen today - that most seem to miss - is not indicative of the business. Using the same discount rate and tax rate for the period 2015-19 paints a completely different picture where Berkeley had an average ROCE greater than 27%! Real returns would have been even higher through that period through lower taxes and lower interest rates. Despite Berkeley trading at over 2.5x book in 2015 the stock roughly doubled between then and Covid.

Obviously, I’m not writing to look back at the past nostalgically to remember a “what-has-been.” But I’m showing you this isn’t an awful business. Just a capital-intensive, cyclical business. The reality is that this is a cyclical at trough prices. It’s hard to see how it gets “worse.”

As Exec Chair, Rob Perrins, wrote in The Times “Today’s crisis is even worse than after the 2008 financial crash.” He blames regulatory costs, taxes and planners for killing development and urges the Labour government to change their ways. He’s right. Capital turns have always been slower than the US. And they’re getting slower.

It was a politically charged article, no question. But I found it very interesting that other homebuilders “blame” other factors, more commonly on the demand side. Persimmon, for example, seem able to increase output but are struggling to sell due to “affordability constraints and increased industry-wide costs.” Bellway reiterated these concerns saying that the government must “address the demand-side constraints.” Barratt and Taylor Wimpey were also mentioned in these articles calling for demand-side stimulus.

Interestingly, Berkeley haven’t really complained on this front. But completed units have swelled from £30m to over £300m between 2015 and 2025. That said, whilst Berkeley have struggled with containing cost of sales operating expenses have consistently been around 6-8% of sales.

Despite all of the above, there is a path to light.

Firstly, inflation seems to be under control and interest rates are set to get cut. More in-line build costs allows Berkeley to maintain margins, stabilise the capital base and borrow cheaply (which will be important for optionality in the BTR segment). Furthermore, politically, the Labour government have pledged to build 1.5m homes which the OBR have revised down to 1.4m. I don’t expect government to get close to that figure but when a government tends to favour an industry, it shouldn’t hurt.

Secondly, looking towards the future, Berkeley’s management have identified and set aside £7b of free cash flow - available to the business from existing reserves and trading activity - to be allocated over the next decade. £2.5b is to be spent on land, £2b is to be spent on shareholder returns, £1.3b is unallocated and £1.2b is to be spent on their BTR platform.

Let’s just pause for a second here because this capital allocation framework is precisely the crux of this investment thesis.

The issue is that management have chucked out this figure and it’s very hard to understand the practicality of this. Pecking order theory is in full effect here. We don’t know exactly how management have determined any of the above. What even is their end goal here?

Analysts and investors both are forced to trust management’s judgement.

Note that pre-tax profit guidance for FY26 is £450 million with FY27 likely to be similar, both of which are lower than 2025 (a poor year, as discussed above).

This is important because if we lazily assume that capex and depreciation is de minimis meaning that tax profits are roughly cash profits (pre-working capital adjustments since management have set aside cash for land) you have a business earning £315m FCF in 2026 and 2027.

(Note that average working capital investments between 2015 and 2025 were about £100m.)

Even the poorest mathematician amongst us can figure out that to get to that £7b FCF figure, between 2028 and 2035 Berkeley will have to throw off about £800m/annum in FCF.

However, markets haven’t reflected this claim either because they missed it (unlikely) or they don’t trust it (highly likely). As I showed you above, such a return would require a rapid acceleration of the London housing market from where we are currently. £800m/annum for seven years seems ridiculous.

Therefore, if we take the £315m for ‘26 and ‘27 and then assume “high but achievable earnings growth mimicking previous booms:

2028: £450m, 2029: £450m, 2030: £650m, 2031: £650m, 2032: £900m, 2033: £900m, 2034: £800m, 2035: £800m

Even in this scenario where earnings pretty much triple over a decade, we still end up short of that “identifiable” £7b FCF!

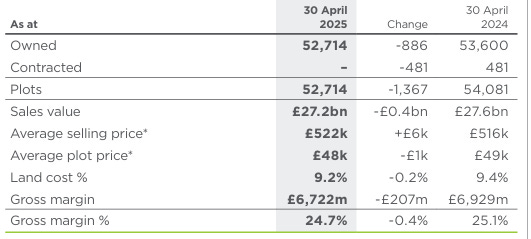

In order to try to understand where this figure came from, I went back to the future gross margin figure. Remember management have estimated future gross margin at £6.7 billion across 52,700 homes. Well, at 8% admin expenses and a 29% effective tax rate (corporate + RPDT), that’s only £4.2b NOPAT, assuming that it’s in line with FCF.

The answer can only come from the pipeline that comprises c.12,000 plots implying that £2.8b NOPAT will come from here.. which seems highly unlikely. At a conservative £500k/plot and a 22% GM, NOPAT totals about £830m. Meaning that I’ve only found £5b “free capital” to be deployed.

That said, if the above were true, Berkeley would only trade at a 14% NOPAT yield through the decade - with net cash unaccounted for - which seems very reasonable.

What is most interesting to me is the BTR platform. Berkeley’s strategy is designed to unlock value by turning its brownfield pipeline into an income-producing platform. Under the Berkeley 2035 plan, up to £1.2b will be deployed over the next decade to deliver 4,000 high-quality rental homes - meeting unmet demand in and around London.

The model is straightforward: Berkeley builds, leases and stabilises assets before deciding the optimal exit route. By holding each building for at least four years beyond completion, Berkeley captures rental growth, establishes a rental premium based on its build quality and ultimately sells (or refinances) a proven, income-generating asset at full investment yield. This approach avoids the typical 20% value erosion seen in forward-funded Private Rented Sector (PRS) deals, where values are fixed two years in advance and priced with risk discounts.

A dedicated BTR team, combining Berkeley leadership with external hires, has already secured six planning consents to refine layouts and amenities for renters. The first scheme launches in spring 2026.

Once stabilised, each asset sits on a platform offering multiple exit strategies: selling individual buildings or curated portfolios, bringing in third-party equity while retaining management, or introducing debt secured against the rental assets. This optionality reduces risk and maximises capital efficiency.

Whilst this is all well and good, it’s theoretical. What are the returns of such a plan?

The strategy unlocks two profit streams.

First, by developing and stabilising the assets themselves, Berkeley avoids the typical 20% discount embedded in forward-funded sales. Since the £1.2 billion build cost represents 80% of full value, the stabilised portfolio is worth roughly £1.5 billion, generating a one-off £300 million development profit.

The second layer comes from a planned four-year hold. Assuming a conservative 3.5% net yield and modest rental growth, the stabilised £1.5 billion portfolio would produce around £220 million in cumulative rental profit over the hold period.

Put together, the plan turns a £1.2 billion capital deployment into roughly £520 million of total cash profit… but time reduces the economic profit. However, given we don’t know the exact details this is a first best guesstimate of what I think is reasonable and is very likely to change in the future as we get more information.

Management are aligned with Executive Chairman, Rob Perrins, owning over 1.25m shares (over £40m) having joined in 1994 and CEO, Richard Stearn, owning 250k shares (over £8m) having joined since 2002.

Management have also been buying shares on the open market recently. Rob Perrins has bought about £1.1m in the last year with Richard Stearn buying over £400k. Do management believe the stock to be cheap even though near-term profits seem to be poor?

Whilst incentives and financial transactions don’t always show the result, they usually indicate where a company may land. And I like what I see.

Of course, I had to know what London was thinking.

As of last week, GS started Berkeley at ‘sell’ with a £37 price target. They pointed to constrained earnings growth given the low viability of residential London development, burdened by slower house price growth, more regulation and low affordability. They also said BTR will take time to contribute to earnings with capital recycling also taking longer.

Maybe Goldman are right. But our time horizons are different.

Risks:

Market conditions do not ease. Inflation persists, interest rates remain high, cost-of-living gets worse. Berkeley do not generate the £7B FCF that their future is built on. They fail to generate sufficient shareholder returns.

BTR model - which is new to Berkeley - has execution errors or is the wrong strategy. However, Berkeley weren’t doing brownfield through their whole history and I’d rather buy a company internally developing something than acquiring something you may not know everything about.

Political tailwinds do not materialise meaning that even with macro improvements, it’s difficult to develop sites.

(It’s also true that brownfield regeneration projects are inherently risky. However, Berkeley have historically been very good at it and if their discipline continues, this risk can stay low.)

To conclude, Berkeley is in dire straits just like the other homebuilders. However, downside is protected because of the balance sheet that management are using to break the market shackles by force (while maintaining £300m net cash for at least until FY26). A savvy capital allocation framework that is geared towards resharpening the business coupled with longer-term political and macroeconomic tailwinds results in a potential compounder at a trough, albeit high-looking, multiple.

Best investing,

HV

(Modelling the future accurately is tricky but management’s track record gives me faith that Berkeley are on the right track. This lack of visibility probably makes Berkeley more of an “uncomfortable” hold compared to some of my other positions because the results aren’t in the current financials yet.)